Simplifying Crypto Structured Products

Overview

In Traditional Finance (TradFi), structured products are essentially managed investment products or packaged financial products whose value is linked to an underlying asset or basket of assets such as market indices, stocks, bonds or a mix of these. Structured products have a pre-defined maturity date, different yield-bearing profiles and payoff curves, ideally sold to investors who want to have exposure to certain thesis in the market. The global structured products market size was over $7 Trillion in 2019, reflecting just 1% of the $700 Trillion derivatives market as per Bloomberg. There are various categories of structured products, however the most common ones are: capital-protected products, yield enhancement products and leverage products.

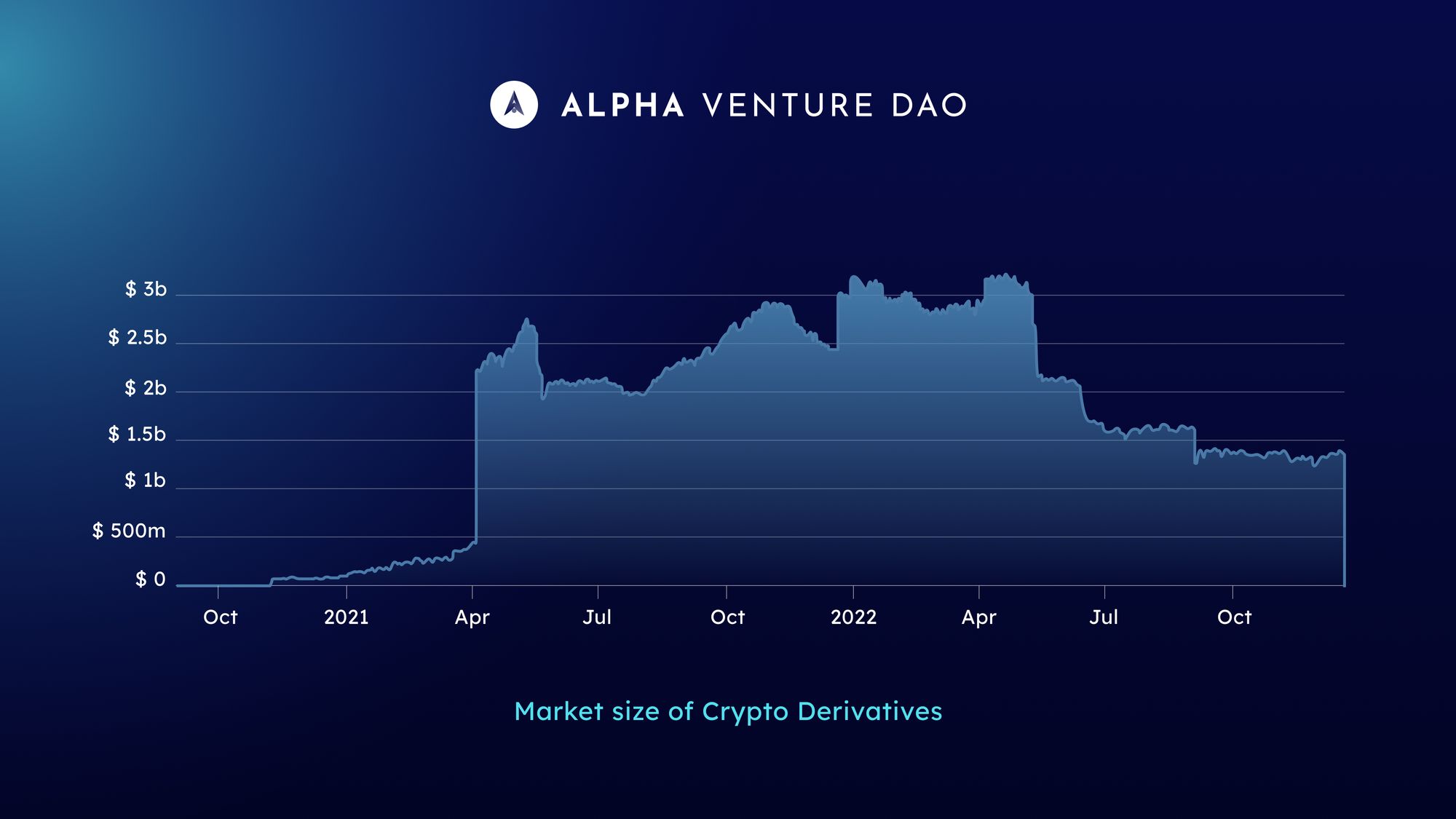

Crypto structured products follow the same concept with a slight difference that the underlying assets are cryptocurrencies such as Ethereum. The concept is to use multiple crypto assets and derivatives to create a unique structure. In crypto, structured products are primarily dominated by option based products. While the exact market size of structured products is difficult to tell, it is interesting to note that the size of the derivatives market is $1.27 billion and the entire DeFi market is $39 billion as of Jan 3, 2023.

In this blog, we will be focusing on five major categories of crypto structured products mentioned below because they have proven to be the most popular among investors and users alike (in terms of Total value locked i.e TVL, number of users, etc.) and have scaled significantly over time.

Landscape

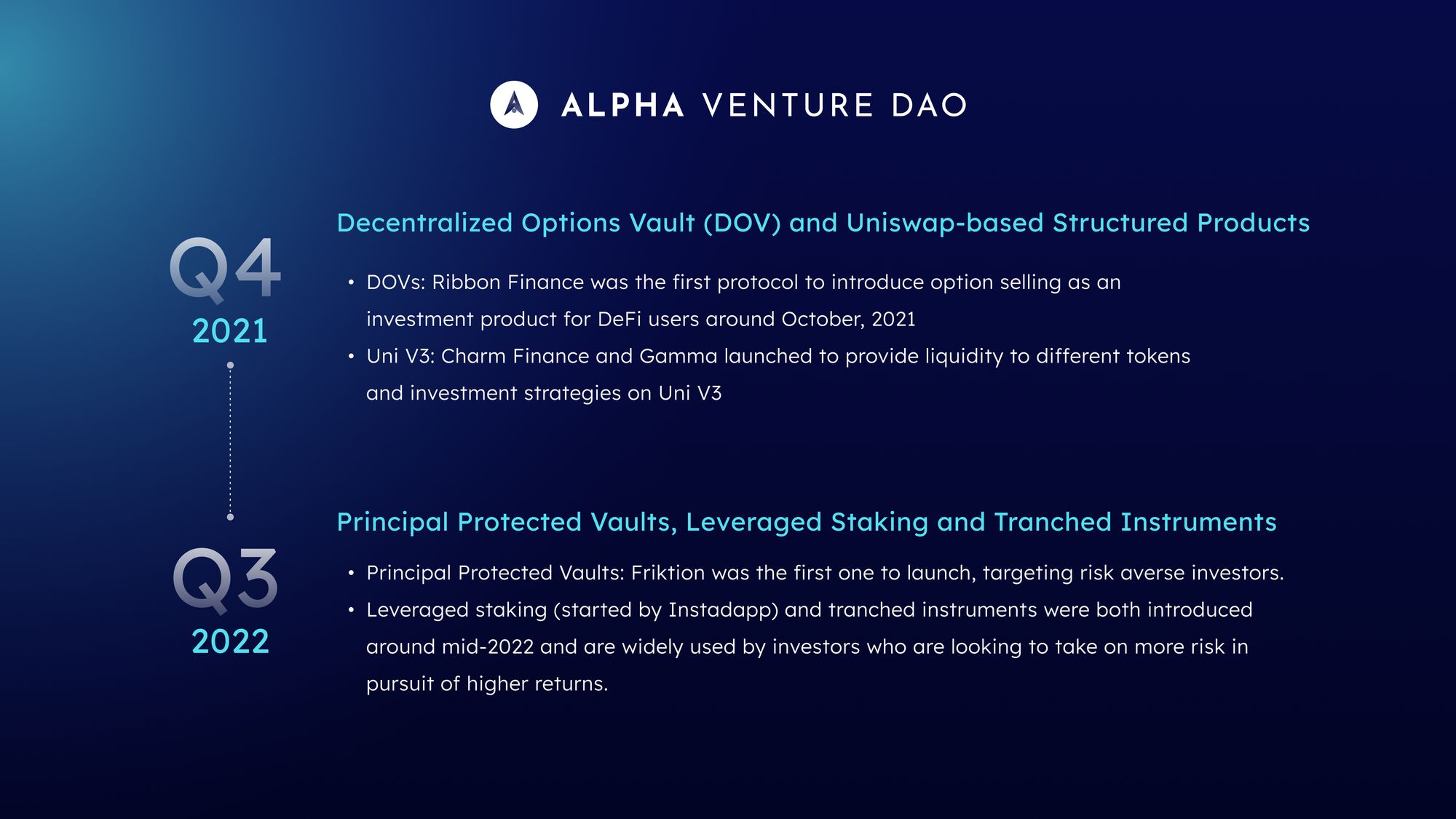

We can see that some of the crypto structured products categories are directly influenced by TradFi structured products (eg. decentralized option vaults & tranched instruments from yield enhancement products, principal-protected vaults from capital-protected products, and leveraged staking from leverage products) and some are unique to crypto such as uniswap-based structured products.

Let’s deep dive into each one below.

Decentralized Option Vaults (DOVs):

Tags: Options, Covered Calls, Cash-Secured Puts.

Description: DOVs are on-chain option vaults, where users are able to buy and sell options. However, to ensure that the vaults are always solvent, users must lock their tokens in the vaults in case their counterparties decide to exercise the options. As a result, only some strategies such as Covered Calls and Cash-Secured Puts are viable for on-chain DOVs. In simpler words, it means selling options and earning the premium paid by buyers. Covered call vaults are a good way to invest in the market downturn because you’re hedging against price decrease, whereas, cash-secured puts are a good way to earn yields in a bullish environment.

How it works: Users stake their tokens into vaults for different options strategies. For Covered Call strategies, users must stake `volatile` assets; whereas, for Cash-Secured Puts, users must stake 'stablecoins'. Each week, the vaults are sold to their counterparties via auctions to determine the price. Normally, the counterparties are market makers, who further sell these options at a higher price in a centralized exchange (like Deribit) and make a low-risk arbitrage profit. One can think of DOVs as matching systems between on-chain option sellers to off-chain option buyers, with market makers as the middlemen. The auction is held on a weekly basis, with the premiums earned by the vaults being compounded to sell more options in the next cycle.

Example protocols: Ribbon Finance (Total TVL: $68..68M), Friktion (TVL: $5.29M), Thetanuts Finance (TVL: $6.67M), etc.

Main user group: Option sellers and option buyers

- Option sellers who have certain theses in the market.

1. For covered call strategies, sellers are expecting their staked assets to at most slightly go up in price.

2. For cash-secured puts, sellers are expecting the volatile assets to at most slightly go down in price. - Option buyers such as market makers who sell these options in centralized exchanges to earn arbitrage spread between the DOV auctioned prices and centralized exchanges' option prices.

Risks/Limitations:

- The yields are not consistent or risk-free, since the option writer holds the underlying asset and takes on the risk of underlying asset’s price movement.

- DOVs are pools-based and the deposits are aggregated. The UX is too simple and inflexible for pro traders.

- DOVs only allow users to sell options, once a week. Also, since decentralized options protocols often lack liquidity, DOVs have to rely on centralized exchanges like Deribit. To tackle these issues, Ribbon Finance has just launched their own decentralized options exchange called Aevo. This exchange is built from the ground-up for pro traders and provides options with different frequencies (daily, weekly, monthly and quarterly).

- Risk level: 3/5; Reward level: 3/5

Principal Protected Vaults:

Tags: Options, Calls, Puts.

Description: Principal-protected vaults emerged to provide risk-averse investors with avenues of generating yields while keeping their capital safe. The principal is invested in safer strategies such as providing liquidity in Curve and then only the returns are invested in riskier strategies such as leveraged trading.

How it works: Principal-protected vaults utilize one low-risk strategy and one high-risk strategy. The low-risk strategy, such as stablecoin LPing and lending, are used on the users' principal deposits for low-return yields. The generated yields are used on high-risk strategies, such as leveraged trading and options trading, to earn even higher yields.

Example protocols: Ribbon Finance (Ribbon Earn’s TVL: $2.93M), Vovo Finance (TVL: $710K), Brahma (TVL: $2.74M)

Main user group: Risk-averse investors who still take LONG exposure on staked assets (e.g. lend ETH) and want to generate more yields at the cost of higher risk, but also do not want to suffer a loss on their initial investment (principal protected).

Risks/Limitations:

- Although the name itself suggests that your principal is protected but that cannot be guaranteed 100% due to various risks involved eg. in the above case, Ribbon’s reliance on centralized market makers for yield can be considered a counterparty risk.

- High risk strat may end up at a loss, implying that the net return may be lower than simply lending/ stablecoin farming

- Risk level: 2/5; Reward level 2/5

Uniswap based structured products:

Tags: Uniswap, Liquidity Provider, Flash Loan, Stablecoin, Impermanent Loss

Description: Automated liquidity provision on Uni v3 pools to auto-adjust liquidity ranges and auto-rebalance farming positions. The initial form of structured products on Uniswap were Uniswap LP pools but as liquidity and incentives dried up, most LP based products turned B2B. Now, uniswap based structured products just act as non-custodial uniswap LP solutions and directly reach out to different protocols for providing liquidity instead. These automated vaults remove the hassle of managing liquidity for projects and help generate more consistent returns.

How it works: These protocols first set up 2 key factors: liquidity ranges and a rebalance threshold. Liquidity ranges determine the concentration of liquidity provided in the pool. The narrower ranges offer higher APY, but come with a higher degree of impermanent loss (IL). Whereas, wider ranges gain less APY, but are less susceptible to IL. Rebalance threshold triggers rebalance when the UniV3 pool price moves further away from the current price and hits the threshold. The position will be rebalanced to a new liquidity range. These protocols conduct backtest experiments to fine-tune these factors for the best risk-reward values. They may also take some management fee.

Example protocols: Arrakis Finance (TVL: $469M), Gamma (TVL: $2.6M), Charm Finance (TVL: $1.52M).

Main user group: Users who love the upside APY of decentralized exchange (DEX) farming and do not want to actively manage position themselves and protocols looking for an efficient way to manage liquidity for their projects.

Risks/Limitations:

- Impermanent loss on both stablecoin and non stablecoin pairs (when rebalancing the position especially in a volatile market) and lower incentives vis-a-vis the risk of providing liquidity to a pool.

- Risk level for stablecoin pairs: 2/5; Reward level for stablecoin pairs: 2/5

- Risk level for non-stablecoin pairs: 3/5; Reward level for non-stablecoin pairs: 3/5

Leveraged Staking:

Tags: Staking, Leverage, Flash Loan, Lido

Description: Staking is generally low risk but also generates low returns. Leveraged staking is used to enhance yields on staking.

How it works: These products use leverage to allow investors to generate higher returns, while maintaining a low risk level.

Example protocols: Instadapp (Total TVL: $1.59B), Oasis DAI (Total TVL: $1.66B), Gearbox (Total TVL: $109.58M)

Main user group: DeFi degens who are comfortable with the risks of taking leverage on basic yield generation mechanisms like staking.

Risks/Limitations:

- Oracle bug/manipulation: eg. what happened with Pyth on Mango Markets

- Depegging of staked assets such as stETH, stMatic: this can happen due to increased sell pressure, such as 3AC collapse or a protocol hack.

- Increased borrow rates/reduced deposit rates: Sometimes the costs to Flashloan-borrow can be higher than staking yields

- Risk level: 3/5; Reward level: 4/5

Tranched Instruments:

Tags: Tranches, Senior Tranche, Junior Tranche

Description: Debt investment opportunities/pools that are cut up into tranches (senior tranche and junior tranche) with different risk/reward profiles. The return associated with junior tranche is more than that with senior tranche, and so is the risk.

How it works: Investors lock in a stable yield by investing in low risk senior tranche since in the unlikely event of a default, senior tranche investors are the ones who get paid first at the expense of junior tranche investors

Example Protocols: Saffron Finance (TVL: $222K) and BarnBridge (TVL: $1.94M).

Main user group: Institutions or risk averse retail investors for senior tranche and DeFi degens for junior tranche.

Risks/Limitations:

- Given most people investing in DeFi are quite far up the risk curve, there isn’t all that much demand for senior tranches, making yields in junior tranches only mildly attractive at the moment.

- Risk level for senior tranche: 1/5; Reward level for senior tranche: 1/5

- Risk level for junior tranche: 4/5; Reward level for junior tranche: 3/5

Conclusion

To conclude, structured products are packaged products that

- meet the need of users whichever the market theses they have (e.g. long/ short/ stable, risk-averse);

- reduce the complexity of investment strategies (e.g. using options and derivatives) to simpler and easy to understand investments (see automated UniV3 farming, senior tranche offering fixed APY); and

- increase capital efficiency (see leveraged staking).

We covered in detail the five major types of structured products in crypto and examples of top protocols in each category. Different types of structured products exist for different market conditions like bull market, bear market, sideways market, etc. and for investors with different risk appetite. To summarize each category:

- DOVs were truly innovative when they first launched and formed a major chunk of the TVL of DeFi options market throughout 2022.

- Principal-Protection Vaults were an extension of the problems with DOVs, and emerged as the next innovative thing to provide risk averse investors with some ways to generate aggressive returns with low risk.

- Uniswap-based structured products emerged because Uniswap V3 requires active monitoring and liquidity management compared to passive LP in Uni V2 or other DEXs.

- Leveraged staking became a really successful primitive in DeFi as the users are already familiar with the concepts of staking and leverage.

- Tranched instruments are very common in TradFi and have the potential to onboard more institutions to DeFi by providing consistent returns with senior tranches.

Looking at the information discussed above, we realized that “Leveraged Staking” as a category is attracting the largest TVL currently. This seems to be because it’s easy to understand from the end user perspective and generates good returns which can be as high as 20%-30% (due to flash loan/ mint by protocols e.g. Maker) in some cases. Now that different sources of yields have dried up and users are looking to fill their urge to degen, leverage staking seems a natural choice. Amongst the other categories, all had attracted huge TVL at one time or the other except “Tranched Instruments', which didn’t gain much traction. This could be because it is too early for tranched instruments in DeFi, given the skepticism of institutions towards crypto and the uncertain regulatory environment. Option Vaults (DOVs and Principal-Protected) need the underlying infrastructure to mature more eg. a deep options market on-chain is still underdeveloped. Once the infra starts maturing, option vaults can prove to be a game changer to bring the next leg of new users to DeFi. Uniswap based structured products are suffering through lower incentives but now that the business model has shifted to B2B as discussed above, we can expect to see more protocols getting involved.

Overall, the Structured Products vertical in crypto is quite nascent and the underlying infrastructure is yet to develop. The yields of structured products need to become sustainable and scalable with assets under management (AUM). Having said that, the future of Structured Products is bright and we believe the protocols that are able to promote transparent and verifiable risks and returns will succeed in the future. As a vertical, there is a lot of room to grow with different structured products for retail and institutions. As the market for crypto structured products continues to evolve, it is likely that we will see the introduction of even more innovative and sophisticated products in the future.

Note: TVLs are as of January 3, 2023

(Source: Delphi Digital, Defillama, OurNetwork)

About Alpha Venture DAO (Previously Alpha Finance Lab)

Alpha Venture DAO is a DeFi venture builder that builds and incubates next generation of DeFi solutions. Alpha previously launched Homora, the world's first leveraged yield farming platform, which attracted over $1.8 billion in total value locked. Alpha Incubate is a bespoke incubation program that serves as a ‘Build Partner’ for founders, offering 1-on-1 bespoke advisory experience to founders and access to more than 100K DeFi community. Alpha was a part of Binance Launchpad and backed by Multicoin Capital, The Spartan Capital, SCB10x, and DeFiance Capital.

Website| Telegram| Discord| Blog| Twitter| Learn| Youtube| Facebook|LinkedIn